Mining in Chile and Its Sustainability.

Author: Laurence Hewick, PhD

Introduction.

South America is a global mining powerhouse, dominating in the production of copper, lithium, niobium, and silver. Chile and Peru lead in copper, while the “lithium triangle” (Chile, Argentina, Bolivia) holds massive reserves. Brazil, a major hub, leads in niobium and iron ore, with significant untapped potential in the Amazon.

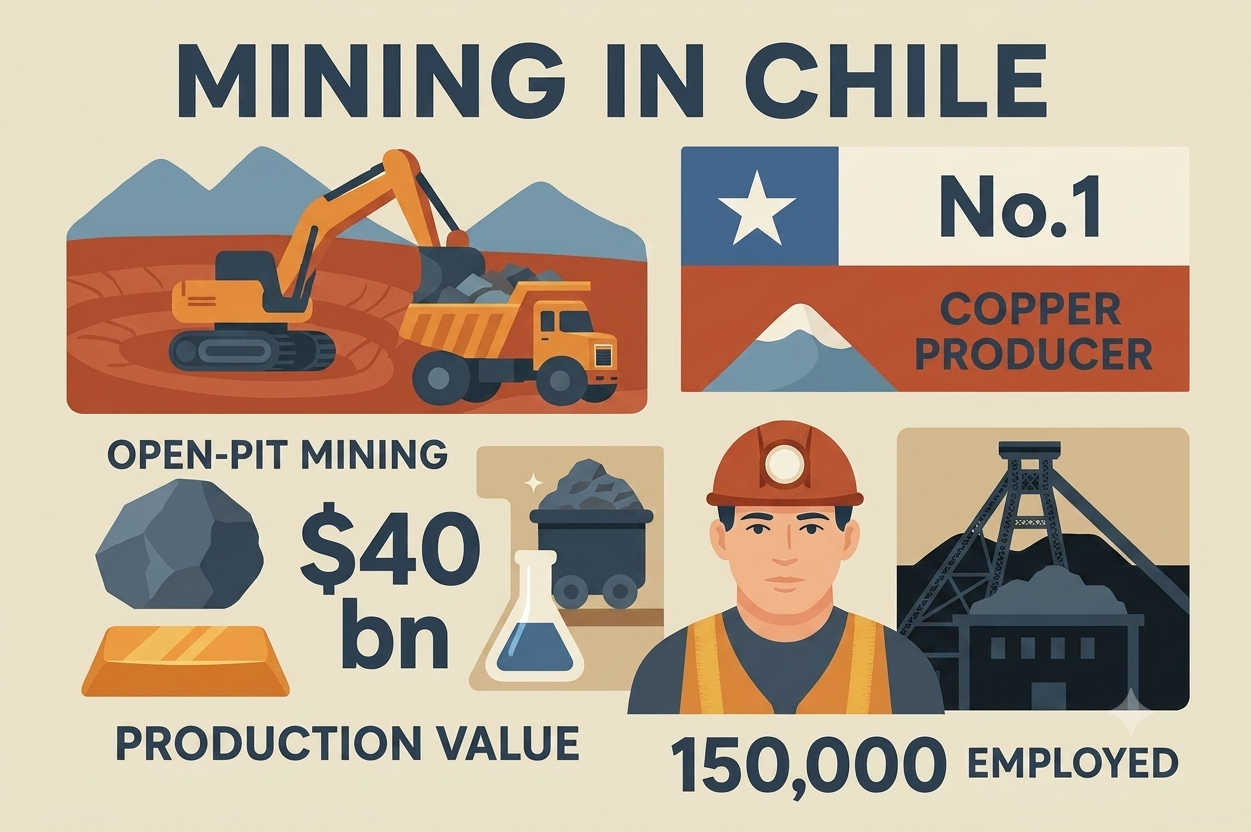

Chile is the world’s leading mining production country holding the top position as the largest producer of copper, iodine, and rhenium, while being the third largest for lithium and molybdenum. Mining, particularly copper, drives the economy, contributing 12% to the GDP and accounting for over 57% of total exports that also amounts to about 24% of global output. The mining sector is facing challenges with declining ore grades and falling production, but major projects are planned for 2024–2033 to fight this challenge.

The mining sector in Chile has historically been and continues to be one of the pillars of the Chilean economy. It is concentrated in 14 mining districts, all of them in the northern half of the country and in the Norte Grande and Norte Chico regions spanning most of the Atacama Desert. Major operations include Codelco the world’s largest copper producer (State owned) but also produces molybdenum, gold, silver and sulfuric acid have made significant investments in sustainability, technology, renewable energy and innovation.

Sustainability of Mining in Chile.

Mining in Chile is undergoing a significant, yet challenging, transformation toward sustainability, driven by renewable energy integration, water recycling, and strict carbon reduction targets. Renewable energy refers to energy derived from natural resources that are replenished at a higher rate than they are consumed. Examples include solar, wind, hydro, biomass, and geothermal energy. These sources are sustainable because they can be used without running out of the resource in question. The benefits of renewables are mostly environmental that reduces greenhouse gas emissions and helps mitigate climate change. Although given the current state of the world in 2026 the benefits also become economic as supply of oil from the Middle East has been greatly reduced due to war.

While mining remains a top economic driver it faces pressure to manage high water consumption in arid regions and reduce significant greenhouse gas emissions. Chile’s mining sector’s current key sustainability trend is focused on renewable energy integration. It is leveraging its geography to power mines with solar, wind, and hydro, aiming for 90% renewable electricity in mining by 2030 and 100% by 2050. Chile is a global leader in renewable energy, generating approximately 70% of its electricity from renewable sources in 2024. The renewables comprise of about 25% from hydro, 20% from solar, 15% from wind and 10% from green biomass. Over half of the electricity for large-scale mining now comes from renewable sources, with companies like BHP and Antofagasta Minerals switching to solar and wind.

Other examples of Chile’s mining sector sustainable environmental strategies include moving their mining fleets from diesel to electric with remote-operated and electric vehicles. Green hydrogen is being explored for heavy transportation and equipment, along with carbon capture technologies that should produce zero emission ming fleets by 2030. The industry is increasing use of desalination plants to reduce freshwater usage, aiming to power these with renewable energy to reduce the overall environmental footprint. The National Mining Policy 2050 and the Mining Council’s agreements set strict, actionable targets to make Chile a leader in sustainable, low-carbon copper and lithium mining. Efforts are also underway to improve tailings management and prioritize circular economy practices in waste management as well as re-process tailings to extract valuable metals like rare earths thus further reducing waste and its carbon footprint. As well as adoption of pyrolysis technology to recover carbon black, steel, and oil from the 27,000 tons of tires generated annually by the mining industry.

Social and Community Efforts.

Chile’s mining firms are increasingly establishing “social licenses” to operate through improved transparency, communication, and agreements with local communities regarding water use and environmental protection. Other examples of the mining sectors efforts to improve relations with its society include efforts to fund education programs, technical training, and supporting local suppliers to ensure the economic benefits of mining reach nearby communities. Advanced technology, such as autonomous vehicles and remote-control rooms, are being deployed to move workers away from high-risk environments, enhancing both efficiency and safety. Working on improving gender diversity, with initiatives like the “Female Entrepreneurs Program” support local women. Finally, the creation of the Center for Innovation and Circular Economy (CIEC) in the Tarapacá region to drive circular business models and high-impact innovation.

Conclusion.

Chile’s mining industry remains a cornerstone of its development, with strong prospects due to the global demand for copper and lithium, renewable energy infrastructures and electric vehicle production. Based on current trends and projections for 2026 and beyond, the future of mining in Chile will be driven characterized by a transition toward sustainability, technology-driven efficiency, and a diversified portfolios that extends beyond traditional copper mining into critical minerals like lithium. While copper will remain the backbone of the economy, the sector faces structural challenges, including declining ore grades and sometimes slow, strict permit processes. Despite these challenges Chile will remain the world’s largest copper producer, with production expected to rise toward a peak in 2027 and again around 2033–2034. The future focus is on expanding existing mines (brownfield projects), such as major upgrades to Escondida and El Abra, rather than new greenfield developments, accounting for 80% of investment through 2033. To offset declining grades, mines are adopting automation, autonomous vehicles, and remote operation centers to improve safety and efficiency.

The government is actively promoting public-private partnerships via its National Lithium Strategy to maximize production, aiming for a significant share of the global lithium market. Beyond lithium, Chile is prioritizing 14 other minerals, including cobalt, rare earths, molybdenum, and rhenium to reduce reliance on copper. A key future strategy involves re-treating tailings and mining waste to extract new metals, converting environmental liabilities into economic assets for the mines and their surrounding communities.

The biggest hurdle is not geological but institutional, with projects requiring hundreds of permits. The new administration taking power in March 2026 is expected to focus on streamlining these to encourage investment. The government further recognizes that Chile will remain a premier mining jurisdiction but faces increasing competition from Argentina and Peru. Maintaining a stable tax and regulatory environment is crucial to securing the $100+ billion in planned investment through 2034. They also recognize that securing a “social license” continues to be essential and maintaining positive community relations remains a top risk factor. The government must also focus on faster permitting and strong ESG (Environmental, Social, and Governance) standards.

References.

The Northern Miner, April 2026

Bloomberg News, March 2026

Mining in Chile, January 2026

International Trade Administration, November 2025

Cochilco Forecast, January 2026

Seeds of Sustainable Development, 2025